Ubezpieczenia to dziwna branża. Klienci kupują ubezpieczenie na wypadek sytuacji, które — mają nadzieję — nigdy się nie wydarzą. Lub jako formę długoterminowej inwestycji. Albo dlatego, że prawo nakłada na nich taki obowiązek. W każdym przypadku powstaje wrażenie, że płacimy za coś, nie otrzymując nic konkretnego w zamian. Nie istnieją częste, pozytywne i przyjemne, ani znaczące interakcje między firmami ubezpieczeniowymi i ich klientami. A kiedy dochodzi do interakcji dzieje się to najczęściej w nieprzyjemnych okolicznościach wypadku lub choroby.

Cyfrowe inicjatywy firm ubezpieczeniowych dotyczą najczęściej sprzedaży oraz zgłaszania szkód, i niewielu innych spraw. My myślimy jednak, że istnieje wiele możliwości stworzenia Value Added Service (usług dodanych) w ubezpieczeniach, tak aby firmy ubezpieczeniowe mogły stać się bardziej obecne i pomocne w codziennym życiu klientów. To jedyny sposób, aby zbudować głębszy związek z marką. W przeciwnym wypadku ubezpieczyciele wpadają w pułapkę konkurowania wyłącznie ceną, i może jakością swoich usług — chociaż większość opinii klientów, które można znaleźć w sieci jest zwykle zła, bo niezadowoleni klienci mają największą motywację do dzielenia się swoim zdaniem.

Oto kilka pomysłów.

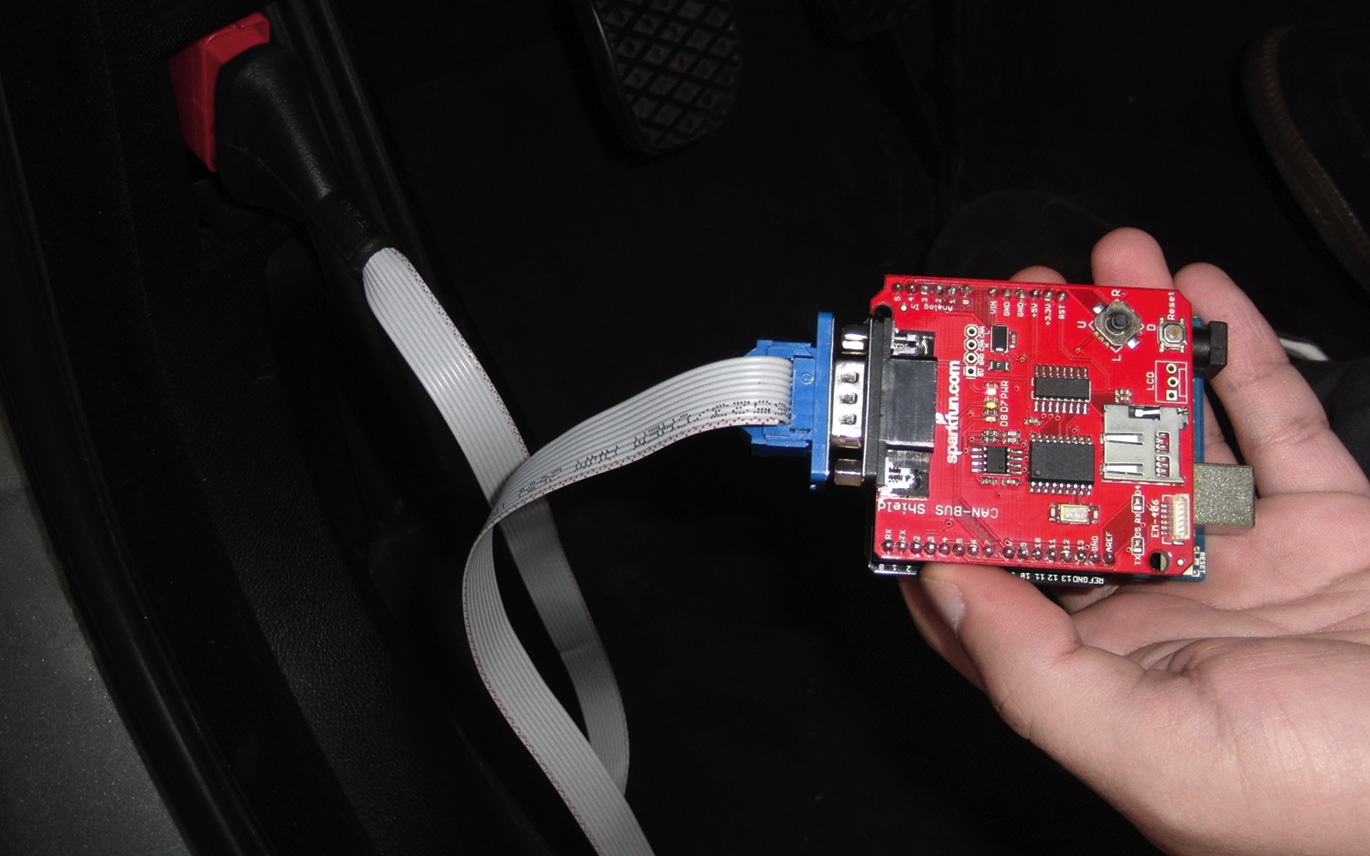

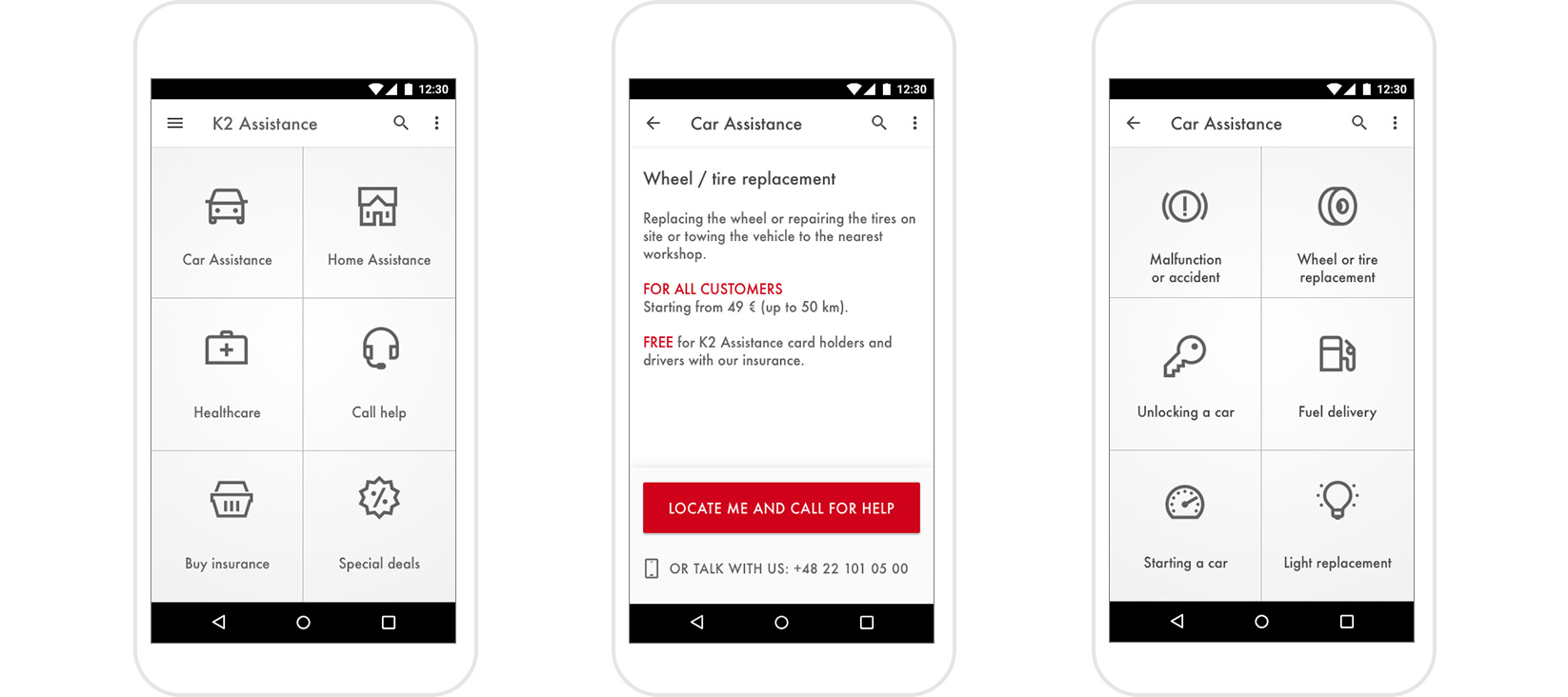

Samochód podłączony do internetu i pomoc dla kierowców.

W 2012 roku wpadliśmy na pomysł urządzenia pozwalającego na podłączenie praktycznie każdego samochodu do internetu. Nasz pierwotny koncept przewidywał, że to urządzenie, podłączone do chmury, mogłoby przewidywać awarię samochodu i automatycznie wezwać samochód naprawczy przygotowany do usunięcia wykrytej usterki. Zaprezentowaliśmy ten pomysł największej firmie ubezpieczeniowej w Polsce — PZU — która się nim zainteresowała, i tak powstało PZU Drive.